UK outlook – Navigating troubled waters

- 01 décembre 2022 (7 minutes)

Key points

- We expect the UK economy to enter recession this year and forecast GDP growth to average 4.3% in 2022, -0.7% in 2023 and 0.8% in 2024

- Inflation should begin to gradually retrace in 2023, falling towards the BoE’s 2% target in 2024

- Interest rates are likely to peak at 4.25% in Q1 2023, but we expect to see the BoE begin to cut from Q4 and across 2024 to end the year at 3%

- Political developments remain important, in particular the Northern Ireland Protocol negotiations remain a risk.

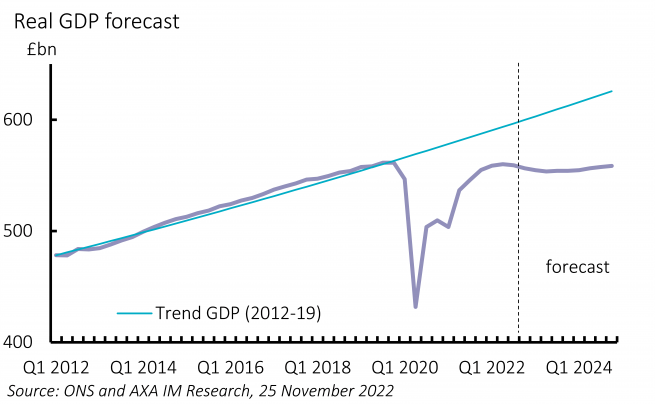

Recession to give way to sluggish recovery

The UK economy has been flashing red for months and the recent decline in Q3 GDP, exacerbated by an additional Bank Holiday, likely marks the beginning of a recession driven by falling consumption, and declines in business and residential investment. We expect this to last around four quarters with a peak-to-trough decline of 1%. Following this, we expect inflation to retrace and alleviate real incomes pressures and for consumption to slowly recover. The slowdown is apparent in levels terms (Exhibit 8) with GDP remaining around its pre-pandemic level. We forecast growth of 4.3% in 2022, -0.7% in 2023 and 0.8% in 2024 (consensus 4.2%, -0.5% and 0.8%).

Labour demand now appears to have turned, lagging declines in economic activity. But a reduction in labour supply has seen unemployment remain low and kept the labour market tight. We see unemployment rising steadily over 2023 and 2024 to peak at 5% towards the end of 2024. We see unemployment averaging 3.6% in 2022, 4.5% in 2023 and 4.9% in 2024.

Energy effects to fade slowly as fiscal stance tightens

Inflation has risen sharply and now stands at 11.1%. We expect a slow decline in the headline rate, with upside contributions from food inflation likely to keep the headline above double digits into 2023. The Government’s decision to extend the energy price cap beyond March next year will help reduce inflation over 2023 as a whole. We forecast Consumer Price Index inflation to average 9.1% in 2022, 7.6% in 2023 and 2.8% in 2024 (consensus 9%, 6.3% and 2.5%).

The Government outlined plans for a sharp fiscal consolidation over the next six years, announcing measures totalling a net £62bn in tightening, despite the impact of energy price caps and recession. This reduces the deficit by £55bn through cuts in spending and increases in taxes. However, energy caps and other cost-of-living top-ups sees the fiscal stance loosen this year, compared to a planned tightening in March. It will now tighten less sharply next year, and the bulk of the tightening now takes place in 2024-2025 and beyond.

BoE first in, first out

The Bank of England (BoE) has increased interest rates by 300 basis points (bps) but the end appears in view. We expect it will increase rates by 50bps in December and February, and 25bps in March to 4.25%. The outlook thereafter, with a growing negative output gap and inflation expected to fall below target towards the end of the forecast horizon, should see the BoE consider loosening policy. We anticipate 25bp cuts in each quarter starting in Q4 2023 bringing rates to 3% by Q4 2024. The precise timing is likely to depend on the scale of labour market adjustment.

Counting down to 2024’s General Election

Negotiations between the European Union and UK on the Northern Ireland (NI) Protocol have resumed as the Government tries to avoid another election in NI. We think second NI Assembly elections by April are likely as the Government seems unlikely to resolve the deadlock. Local elections will also be held in May 2023 but a General Election should be held in 2024. Opinion polls currently suggest a Labour win. However, in contrast to recent elections, both main parties have been forced back to the political centre ground and economic orthodoxy, meaning the next election should be the least economically damaging for a decade.

Nos perspectives pour 2023

À quoi les investisseurs doivent-ils s'attendre en 2023 ?

Perspectives régionales (en anglais)

Perspectives 2023

Nos experts partagent leurs pespectives sur l'année à venir

En savoir plus

Mentions légales

Investir sur les marchés financiers comporte un risque de perte en capital.

Cette vidéo est exclusivement conçue à des fins d’information et ne constitue ni une recherche en investissement ni une analyse financière concernant les transactions sur instruments financiers conformément à la Directive MIF 2 (2014/65/UE) ni ne constitue, de la part d’AXA Investment Managers ou de ses affiliés, une offre d’acheter ou vendre des investissements, produits ou services et ne doit pas être considéré comme une sollicitation, un conseil en investissement ou un conseil juridique ou fiscal, une recommandation de stratégie d’investissement ou une recommandation personnalisée d’acheter ou de vendre des titres financiers.

Du fait de sa simplification, ce document peut être partiel et les opinions, estimations et scénarii qu’il présente peuvent être subjectifs et sont susceptibles d'être modifiés sans préavis. Aucune garantie ne peut être donnée quant à la réalisation effective des scénarii présentés. Ce document ne contient pas les informations nécessaires à la prise d’une décision d’investissement.

AXA Investment Managers Paris – Tour Majunga – La Défense 9 – 6, place de la Pyramide – 92800 Puteaux. Société de gestion de portefeuille titulaire de l’agrément AMF N° GP 92-008 en date du 7 avril 1992 S.A au capital de 1 421 906 euros immatriculée au registre du commerce et des sociétés de Nanterre sous le numéro 353 534 506.

Avertissement sur les risques

La valeur des investissements, et les revenus qu'ils génèrent, sont sujets à des variations, ce qui peut engendrer une perte totale ou partielle du capital initialement investi.